Most people think diversification is the financial equivalent of wearing a seatbelt. Safe. Sensible. Something you do without thinking too hard about it.

But here’s the uncomfortable truth nobody tells you: the way most people diversify doesn’t reduce risk. It hides it.

The Illusion of Safety in Numbers

Picture two investors. Investor A owns 8 stocks. Investor B owns 40 stocks across “different” funds. On paper, Investor B looks like the responsible one. The grown-up. The one who read a book about investing instead of watching a YouTube video at 1am.

But when the market crashed in 2008, Investor B’s portfolio fell just as hard as Investor A’s. Why? Because Investor B wasn’t actually diversified. He was diluted.

This is the distinction almost nobody draws, and it’s the reason so many people get blindsided by losses they thought they’d protected themselves against.

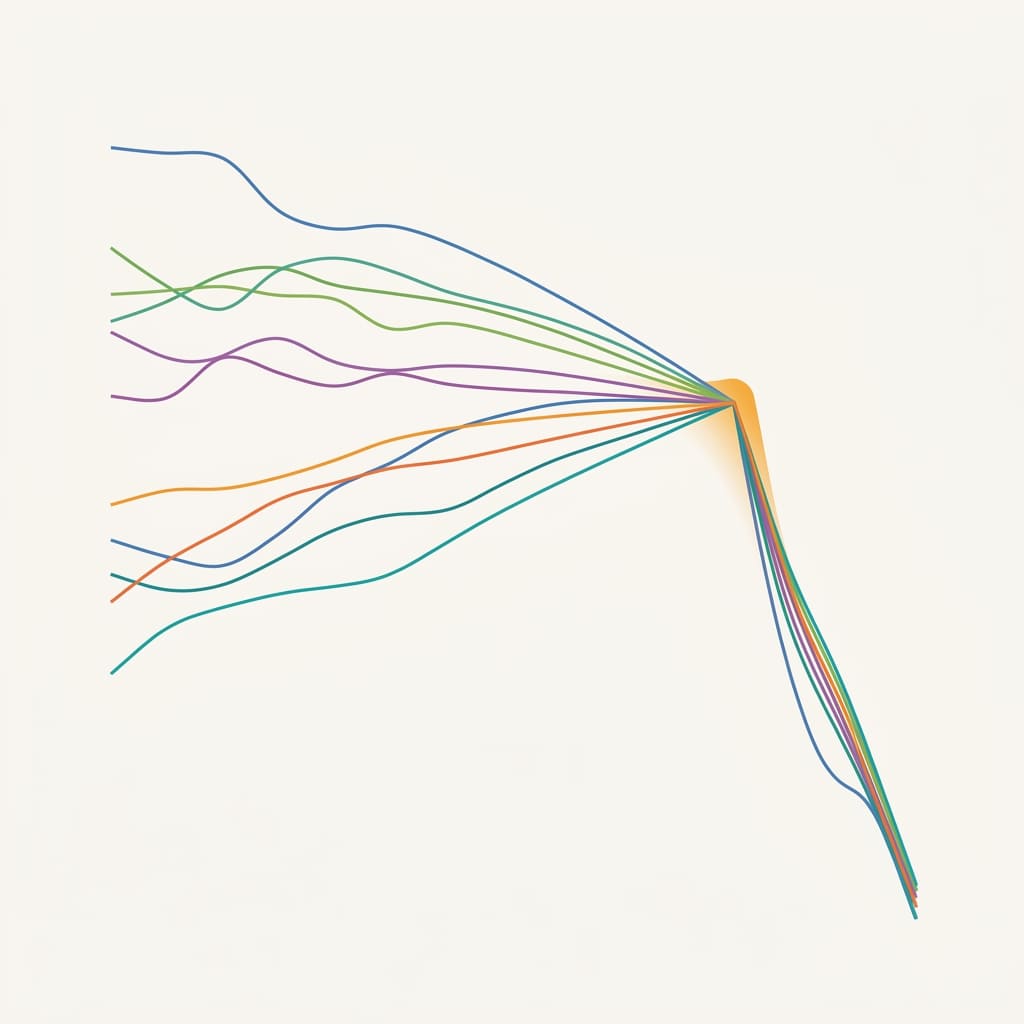

Diversification works when your assets respond differently to the same event. Dilution happens when you own more things that all respond the same way. Forty tech-heavy mutual funds with overlapping holdings aren’t 40 different bets. They’re one bet, dressed up in a costume of forty.

Here’s the part that should bother you: most “target date” and “balanced” mutual funds marketed as instantly diversified are often packed with overlapping large-cap U.S. equities. You can check this yourself in seconds using a tool like Morningstar’s Instant X-Ray (https://www.morningstar.com), which reveals your actual sector overlap. Most people never do.

But that’s not the most important part.

The Hidden Correlation Trap

Here’s a concept that rarely gets discussed outside of finance textbooks: correlation isn’t fixed. It changes, and it changes at the worst possible time.

During calm markets, asset classes tend to drift apart, giving the appearance of healthy diversification. Bonds zig while stocks zag. International stocks behave differently than domestic ones. Real estate marches to its own rhythm.

Then a crisis hits, and something strange happens. Correlations spike toward 1. Everything starts falling together. The very moment you need diversification to work is the moment it often fails you most.

This phenomenon has a name in behavioral finance circles: correlation convergence. Investors who built portfolios assuming historical correlations would hold steady got a brutal lesson in 2008 and again in March 2020, when supposedly unrelated assets all dropped in near lockstep.

This creates a hidden effect few investors notice until it’s too late.

Why Your Brain Loves Fake Diversification

There’s a psychological reason this trap is so easy to fall into, and it has nothing to do with intelligence.

It’s called the diversification heuristic, a term coined by behavioral economist Shlomo Benartzi. His research found that when people are given more investment options, they tend to spread their money evenly across whatever is offered, regardless of what those options actually contain. Give someone five stock funds and one bond fund, and they’ll often put roughly equal money into each, including the five overlapping stock funds.

The brain isn’t analyzing risk. It’s pattern matching to a feeling of balance.

This single bias might explain why so many retirement accounts are quietly concentrated in ways their owners would never knowingly choose. You can read about the original research summarized on sites like Investopedia (https://www.investopedia.com) if you want to see how deep this rabbit hole goes.

Oddly enough, this same pattern shows up in everyday financial decisions far beyond the stock market, in the exact mistakes that quietly cost people years of compounding. We unpacked the full list of these silent wealth killers in 11 Investing Mistakes That Secretly Delay Your Wealth by a Decade, and one of them is almost identical to the diversification trap, just wearing a different disguise.

The Number That Actually Matters

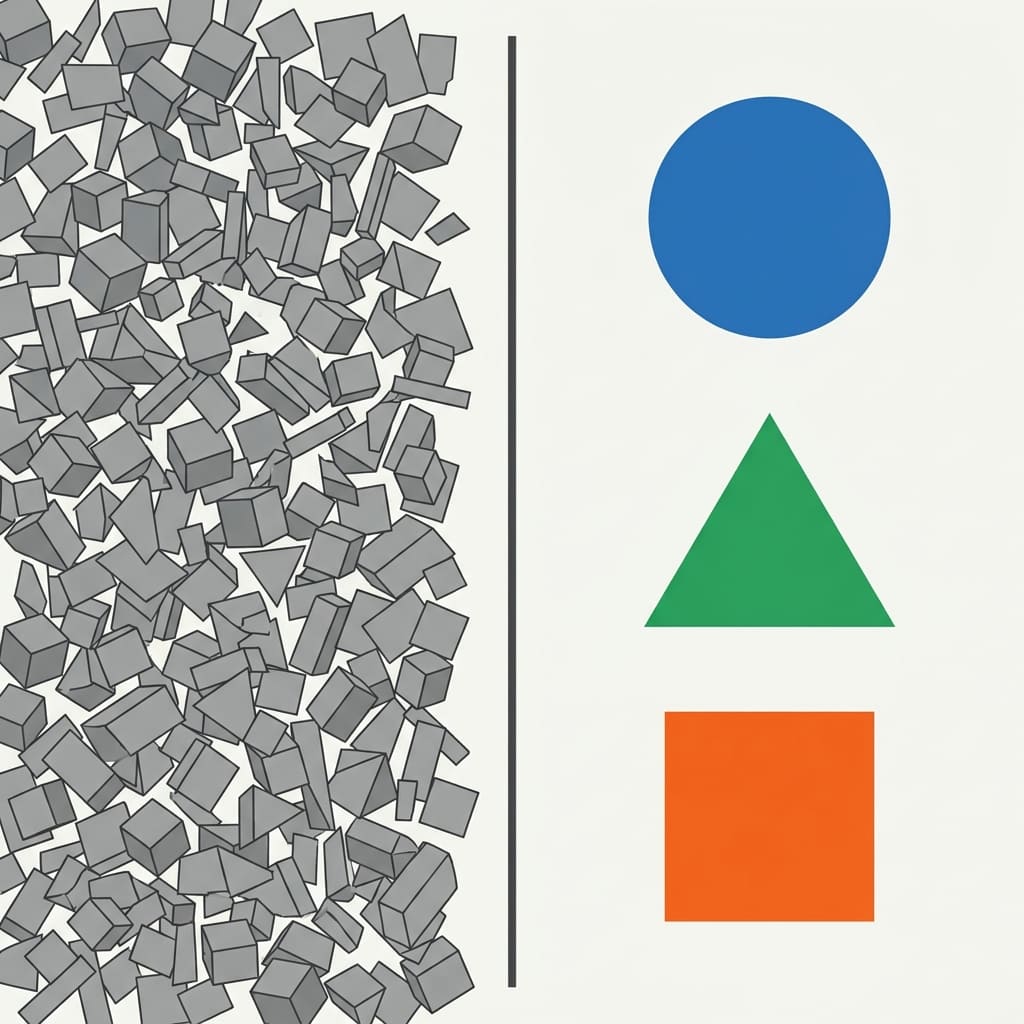

If counting your holdings doesn’t tell you how diversified you are, what does?

Sophisticated investors look at something called factor exposure instead of headline count. A factor is an underlying force driving returns, things like interest rate sensitivity, economic growth dependency, or exposure to a single currency.

Two completely different sounding investments, say, a REIT fund and a regional bank stock, can both be quietly betting on the same factor: interest rates. Own both, and you don’t have diversification. You have a leveraged bet on one variable, split across two tickers.

This is the real advantage that separates institutional investors from everyday ones. It isn’t access to secret stocks. It’s the discipline to ask “what is this actually exposed to?” instead of “how many different things do I own?”

The Three-Asset Portfolio That Outperformed Forty

Here’s a real-world example that tends to stop people mid-scroll.

Researchers studying portfolio construction have repeatedly found that a simple three-fund portfolio (a total U.S. stock index, an international stock index, and a bond index) often matches or beats portfolios stuffed with dozens of overlapping funds, once fees are accounted for. The Bogleheads community (https://www.bogleheads.org), built around this exact philosophy, has documented this pattern for years using real account data shared by its members.

The reason isn’t magic. It’s that three carefully chosen funds with genuinely low correlation can offer more real diversification than forty funds that all secretly move together.

This is the investing paradox almost nobody talks about: more holdings can mean less protection. Complexity creates the feeling of safety while sometimes quietly removing it.

The Decade Most People Lose Without Noticing

There’s a slower, quieter cost to fake diversification that doesn’t show up in a single bad year. It shows up over ten or twenty.

When your portfolio is secretly concentrated, you don’t just risk a bigger crash. You risk something sneakier: a return pattern that looks “diversified enough” to avoid scrutiny, while underperforming a genuinely diversified portfolio year after year due to fees layered across all those redundant funds.

Most people stop their analysis at “am I diversified.” That’s a mistake. The more useful question is “what is this costing me in overlap and fees, and what would I gain by actually fixing it.” That overlooked second question is the centerpiece of 11 Investing Mistakes That Secretly Delay Your Wealth by a Decade, because the math on compounded fee drag is far more brutal than most people expect once you actually run the numbers.

What Actually Reduces Risk

So what does real diversification look like in practice?

It starts with asking three questions before adding any new investment:

- What economic conditions make this investment rise?

- What economic conditions make this investment fall?

- Do I already own something that rises and falls under those same conditions?

If the answer to that third question is yes, you’re not diversifying. You’re duplicating.

Genuine diversification often means owning assets that feel uncomfortable together. Bonds when stocks are euphoric. International exposure when domestic markets feel unstoppable. Cash when everyone insists cash is “dead money.” Comfort and protection rarely arrive in the same package.

This is exactly the kind of overlooked opportunity that doesn’t look exciting on the surface, the kind investors skip past because it lacks the thrill of a hot stock tip. We dig into several of these unglamorous but powerful moves in 7 Wealth-Building Opportunities Most People Ignore Because They Don’t Look Exciting, and the pattern connects directly back to everything in this article.

The Quiet Habit of People Who Build Real Wealth

There’s a thread connecting everything in this article: the investors who build lasting wealth aren’t the ones chasing the most holdings or the cleverest sounding strategy. They’re the ones who keep asking uncomfortable questions about what they actually own and why.

That habit, more than any specific stock pick, tends to separate people who compound wealth quietly over decades from people who feel busy and diversified while quietly standing still. It’s a mindset shift more than a tactic, and it’s woven through The 11 Wealth-Building Rules I Wish Someone Had Told Me at 20, including the rule that most twenty-year-olds (and plenty of fifty-year-olds) never learn until it’s cost them real money.

The Real Takeaway

Diversification was never about owning more things. It was always about owning different things, for different reasons, that respond differently when the world throws a surprise at you.

Count your correlations, not your holdings. That single shift in thinking will do more for your risk management than any amount of additional funds ever could.

One Last Thought Worth Sharing

If you’ve ever felt confident about your portfolio simply because it “looked” diversified, you’re not alone. Most investors have fallen for this at some point, including plenty who manage money professionally.

If this reframed something for you, send it to the one friend who’s always bragging about how many funds they own. They’ll either thank you or argue with you, and either way, they’ll be thinking about their portfolio differently by tomorrow.